The impact of high inflation and interest rates on Canadians and their employers

Welcome to the spring 2023 edition of GO with Eckler. In this issue, we’ll explore the headline-grabbing topic that’s dominating boardroom and living room conversations around the globe: high inflation. We’ll focus on the impact of rising inflation and interest rates on Canadian employees and their employers – and provide insights on what employers can do to mitigate financial stress in the workplace.

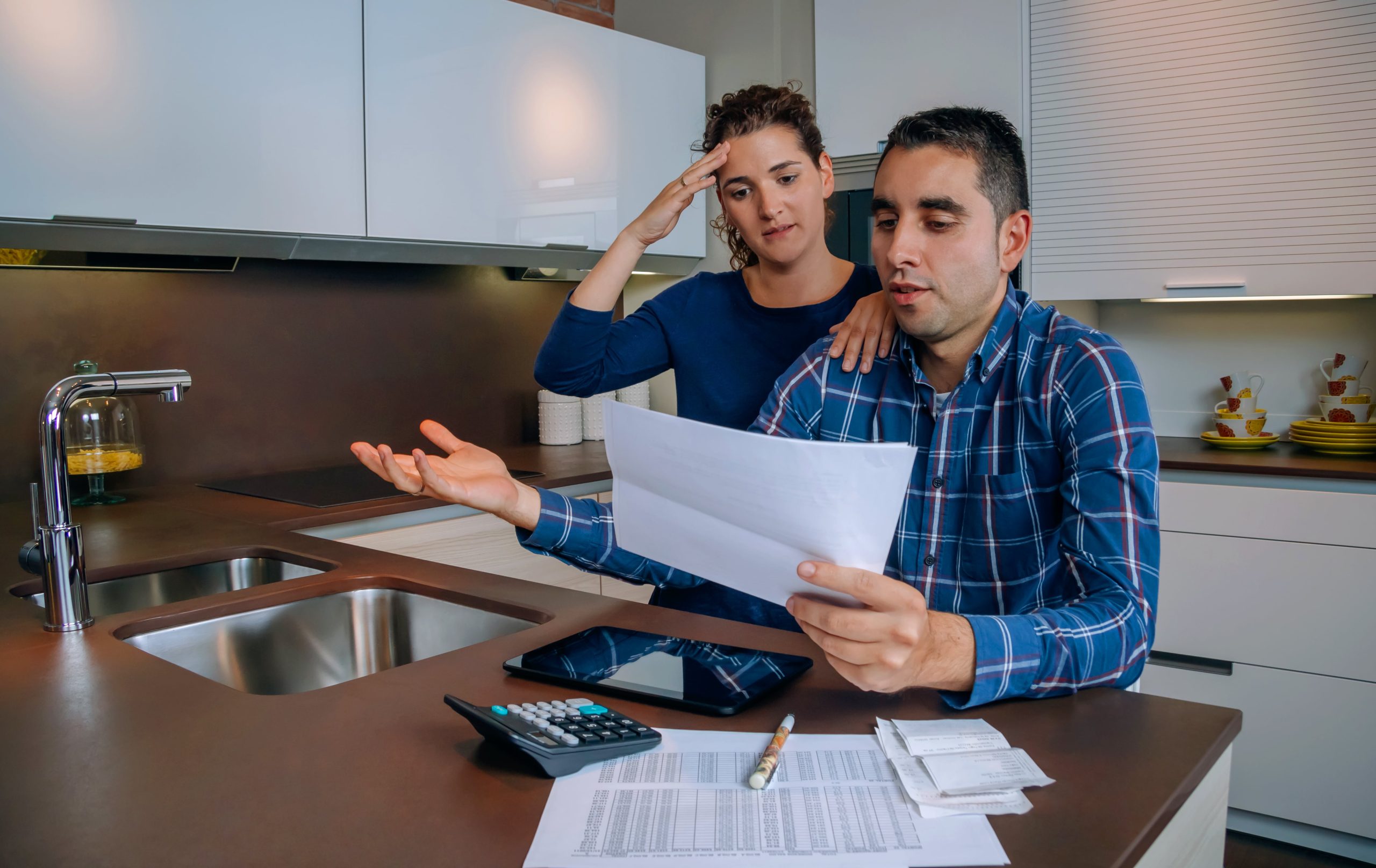

A recipe for financial stress and workplace distraction

Add one scoop of rising food and utility costs with a dollop of higher rent and mortgage payments; stir in a dash of increased credit card debt; combine a heaping cup of rising borrowing costs with diminishing market returns and you’ve got a perfect recipe for financial stress. Unfortunately, we don’t have to wait for this cake to bake before we get a taste of it.

Add one scoop of rising food and utility costs with a dollop of higher rent and mortgage payments; stir in a dash of increased credit card debt; combine a heaping cup of rising borrowing costs with diminishing market returns and you’ve got a perfect recipe for financial stress. Unfortunately, we don’t have to wait for this cake to bake before we get a taste of it.

According to a recent survey1, more Canadians are living pay cheque to pay cheque, have more credit card debt, and are saving less for retirement with more than one-third reporting that they may never be able to fully retire. Canadians are also reporting their highest levels of financial stress since the 2008 recession and 82% say they spend time at work worrying about personal finances.2 The cost of that workplace distraction? An estimated $40B in 20223.

A closer look at impact by age group

While the financial woes and resulting stress is alarming for all Canadians, the impact of high inflation and interest rates is felt differently among age groups. Younger Canadians, who may have experienced poor market returns are likely going to be able to recoup some of those losses as they have a longer time to invest their saving before drawdown at retirement. The rising cost of living and out-of-reach housing prices in most Canadian cities, however, has meant that they may have also had to delay buying homes.

Middle-aged Canadians may have less time to recoup investment portfolio losses and also likely trying to manage larger mortgage costs. However, they are also likely to have gained significant equity in their homes which may allow them to weather the storm a little better. Others may be forced to delay retirement or take on additional risk in the coming years in an attempt to get back on track with savings goals.

Those who are already retired, or who are nearing retirement, do not have the benefit of the same time horizons and are less likely to be able to recoup losses through a market uptick. However, they too are likely to have significant equity in their homes. Those without may find themselves delaying retirement or going back into the workforce.

Those who are already retired, or who are nearing retirement, do not have the benefit of the same time horizons and are less likely to be able to recoup losses through a market uptick. However, they too are likely to have significant equity in their homes. Those without may find themselves delaying retirement or going back into the workforce.

Impact on the bottom line

While inflation has come off its 2022 high, there is still a way to go to reach the Bank of Canada’s target rate of 2% and, while some economists are predicting we will see interest rate cuts by the end of this year, the Bank of Canada has given no indication that they are planning to do so and have said that they have not ruled out future rate increases if needed.

Canadian workers are cash-strapped and stressed out – and there is little indication that full relief will come anytime soon. For Canadian employers, the residual impact will linger for far longer as employees struggle to recoup losses and get back on track with savings and retirement goals. In fact, the Financial Consumer Agency of Canada estimates employee financial stress costs employers an average of $1,000 per employee per year. By all accounts that is a sobering figure. Unfortunately, it gets worse. This figure does not include the additional financial impact of increased use of sick time, disability costs for soaring mental health claims, or decreased productivity. Clearly, financial stress is no longer simply a “personal matter.”

Workplace financial wellness initiatives can help

If you are a regular reader of this newsletter, you will have no doubt found some nuggets of truth and wisdom in our series on how to build a comprehensive financial wellness program in the workplace. Some of you may have already started on the path to building a program and some may still be considering it. No matter where you are on the journey, there are initiatives that most organizations can take now (with minimal effort) to support employee financial wellbeing – and the organizational bottom line.

Know your employees and provide meaningful support

Your employees likely comprise a varying demographic by age, family status, financial situation and retirement goals. Perhaps your younger employees need some tips on how to budget. Those nearing retirement may benefit from more targeted and personalized advice from a certified financial planner. By tailoring your initiatives to each life stage, your employees are more likely to engage and get what they need from it – and your organization is more likely to see a return on the investment.

Communicate, communicate, communicate

Let your employees know you understand and want to support them. Clear and honest communication from people they know and trust can be a powerful thing. Done well, communication can both educate and inspire employees to take a more active role in their personal financial wellbeing. If you already have a company blog or regular newsletter, adding a message or two about where to find free financial wellness and literacy resources (see our list below) is sure to be appreciated. If you have a larger budget to spend, working with a professional communicator can help ensure that you are developing and delivering targeted and effective communication.

Get help from an accredited, unbiased workplace financial wellness expert

You likely don’t have the internal expertise or knowledge to deliver a financial wellness program. Working with an accredited professional ensures that your employees are getting expert support. It also helps develop credibility and “buy-in.” When employees know they’re receiving information from a professional, they are more likely to engage in the program and achieve their goals. And, because virtually no one likes an “upsell,” we believe a financial wellness expert should be solely focused on your employees’ financial wellbeing and not on selling products or services. Whether webinars, in-person workshops, or one-to-one guidance, an accredited financial wellness expert can help you develop and deliver targeted education that makes sense for your employees – and your organization.

Free resources from trusted sources

If you don’t have the resources to develop your own initiatives, or the budget to work with an external financial wellness consultant, there are some great free resources from trusted sources that can help bridge the gap until you do. We have listed some of them below.

- Canada Mortgage and Housing Corporation – Tools, information, and tips on buying, owning, and renting a home.

- Financial Consumer Agency of Canada – Information and resources to help Canadian consumers better understand financial products and services.

- Chartered Professional Accountants Canada – Educational resources to improve financial literacy in Canada.

- Credit Counselling Society – A Canadian non-profit organization dedicated to providing free credit counseling, low-cost debt solutions, and education to help people manage their money better.

We hope this issue of GO with Eckler has provided some timely information on the impact of rising inflation and interest rates on Canadians and their employers, and provided some insights on what employers can do mitigate the impact of employee financial stress in the workplace.

GO with Eckler is a quarterly newsletter to help employers and plan sponsors support financial wellness for their employees and plan members.

12022 BDO Canada Affordability Index.

2Ceridian, in partnership with the Financial Wellness Lab of Canada.

314th Annual National Payroll Association Survey of Working Canadians, 2022.

Please contact your Eckler consultant if you would like to learn more about supporting finances.

![]()

![]()

![]()