Strong Beta. Weak Alpha

By: Devin Forbes, CFA, Associate Director, Investment

Driven mainly by a small cohort of index constituents, equity markets in 2025 delivered strong headline returns (The “beta”). This made it difficult for active equity managers (where we expect the “alpha” to come from) — especially in North America. Outside North America, index dominance was less pronounced and active managers performed better.

This analysis focuses on where index leadership was strongest and why that mattered for relative performance. Index returns are evaluated in the context of active manager universes, with percentile rankings highlighting how difficult it was for managers to keep pace with benchmarks.

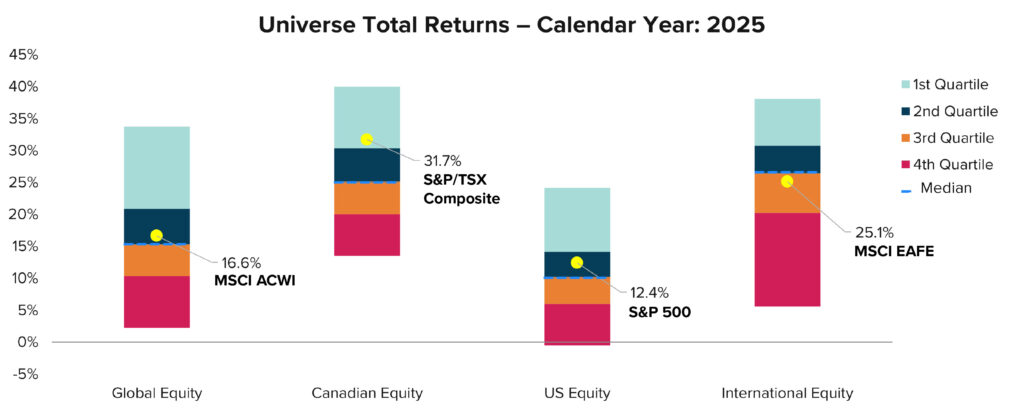

Globally, the MSCI ACWI outperformed the median manager, landing in the second quartile mainly due to its strong U.S. weighting. In Canada, the S&P/TSX Composite led the top quartile, and the S&P 500 was also strong, highlighting challenges for active managers in North America. However, international equities differed. The MSCI EAFE trailed the median manager, indicating that, on average, active management added value abroad. These results show that index-driven performance prevailed in North America, while international markets favored stock selection. This underscores how market structure, not just manager skill, influenced regional outcomes, especially given differences in index concentration.

Index Concentration as a Structural Driver

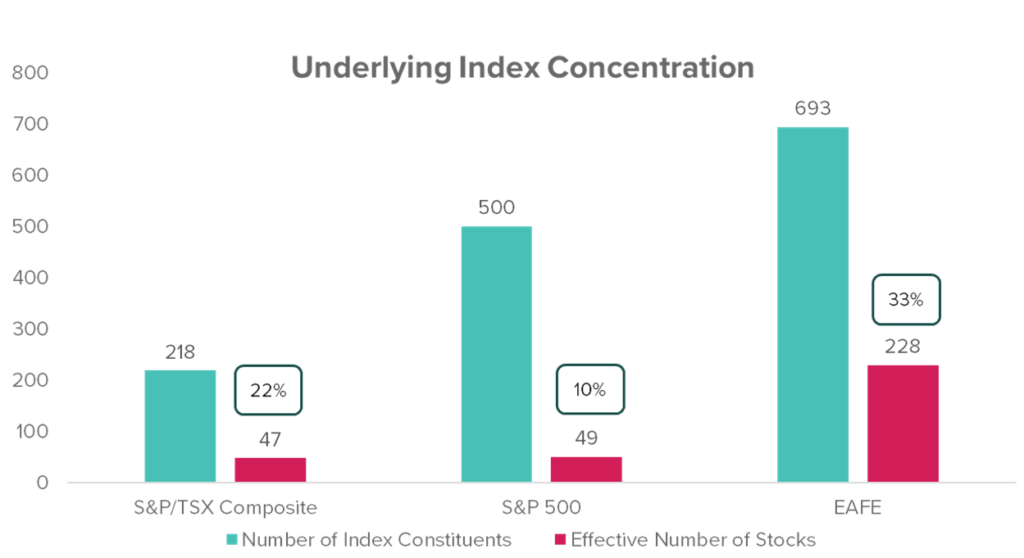

A central explanation for the divergent regional outcomes in 2025 lies in index concentration. Concentration can be measured using the Herfindahl‑Hirschman Index (HHI), which captures how index weights are distributed across constituents. To make this more intuitive, our analysis uses the inverse of HHI to calculate the effective number of stocks—the number of equally weighted holdings required to replicate the index’s concentration profile.

While North American indices like the S&P 500 and S&P/TSX Composite have many constituents, relatively few stocks drive most of the risk and returns — often just a handful of mega-cap names. In contrast, international markets such as those tracked by the MSCI EAFE index feature higher effective breadth, with returns spread across more stocks, reducing the impact of any single company or sector.

This structural difference matters for active managers: in low-breadth markets, performance depends heavily on large index components, while high-breadth markets offer more opportunities to add value through stock selection. Understanding these patterns is essential before analyzing how they have affected active manager outcomes over time.

How Concentration Translated into Active Underperformance

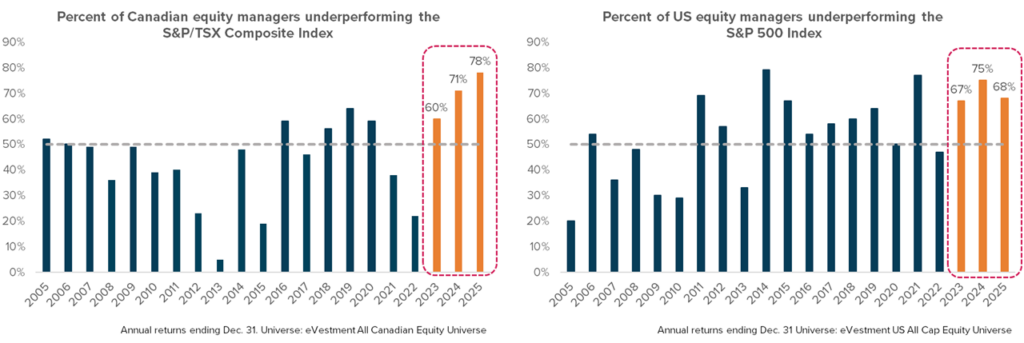

The impact of index concentration is evident in long‑term active manager results, particularly in Canada and the United States. Over recent years, the proportion of managers underperforming their benchmarks has increased in both markets, consistent with periods of narrow leadership and elevated concentration.

Active management has long faced challenges in the U.S., given high market efficiency, extensive analyst coverage, and broad institutional ownership. Recently, dominance by mega-cap tech stocks has further limited opportunities, making portfolio outcomes heavily dependent on exposure to these leaders.

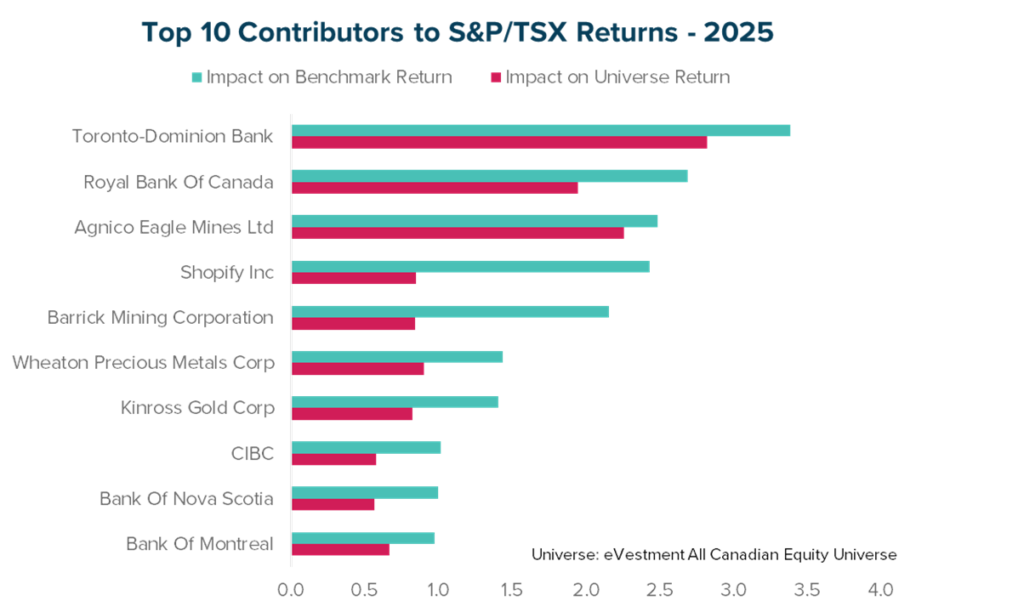

Canada, by contrast, has typically favored active strategies due to sector variety and less efficient pricing. However, in 2025, index gains were concentrated among a few contributors: major banks drove much of the returns, Shopify surged on strong earnings, and gold and mining stocks saw notable gains.

Many active managers held fewer of these exposures due to valuation, volatility, and risk controls. This led to notable underperformance, as the top ten S&P/TSX Composite contributors made up approximately 30% of the index weight and accounted for over half of the index returns, but had less presence in active portfolios. This result reflects concentrated market leadership outweighing diversified strategies, making performance hinge on just a few stocks.

Implications for Evaluating Active Equity Managers

The 2025 market illustrates the need to separate structural effects from manager skill when assessing active equity performance. Recent underperformance mostly stems from index concentration, not declining management ability.

Attribution analysis helps investors distinguish between results caused by market factors and those due to manager choices like stock selection or sector bias.

Reacting solely to index performance can lead to poor timing because shifting to passive strategies during periods of high market concentration increases exposure to a few dominant stocks and reduces diversification.

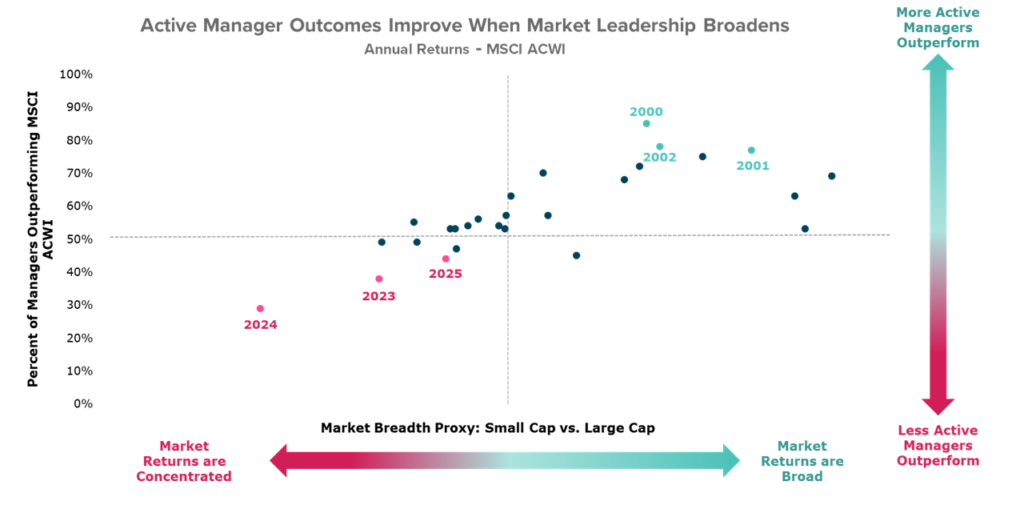

Historically, narrow market leadership limits opportunities for active outperformance, while broader markets benefit stock pickers. Investors should use this time to review portfolio structure, compare active and passive roles, and ensure manager approaches align with their stated philosophy and risk measures.

Market history suggests that narrow leadership is unlikely to persist indefinitely. When market breadth eventually broadens, the opportunity set for active management typically expands, creating more favorable conditions for disciplined stock selection.

Periods like this can be useful for assessing process discipline, as managers face pressure to chase index leaders that may conflict with long-term risk controls.

Any portfolio changes should therefore be client‑specific and forward‑looking, grounded in a clear understanding of market structure rather than short‑term relative results.