Currency crosswinds: How U.S. dollar ups and downs shaped Canadian investor returns

August 2025

From tailwind to headwind

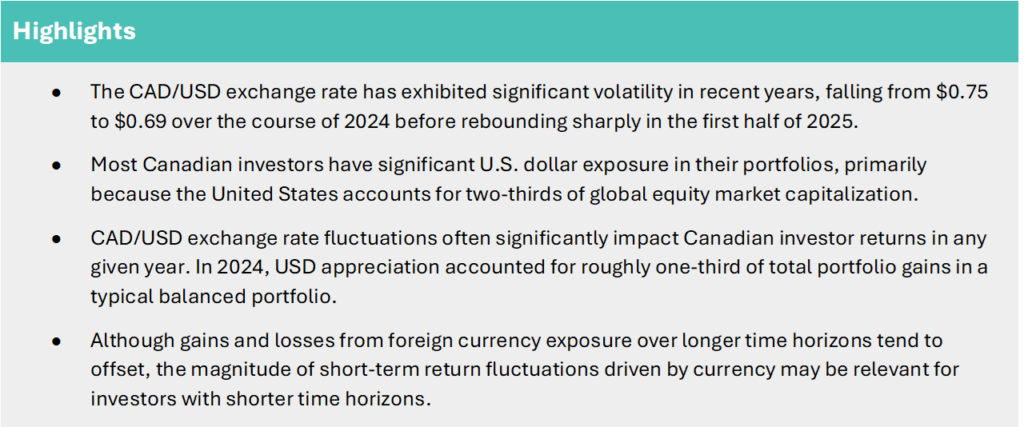

For all the attention garnered by stock market concentration within the “Magnificent 7” group of stocks, an even narrower contributor significantly impacted most Canadian investor returns in 2024: the U.S. dollar.

Canadian investors experienced a 36.4% return from the S&P 500 Index last year, as compared to “only” 25.0% for U.S. investors. For both sets of investors, price appreciation and dividends from the underlying companies accounted for approximately 25% of total index returns. However, Canadian investors received an additional boost on their USD-denominated holdings, as the value of $1 USD invested in the index rose from $1.32 CAD to $1.44 CAD over the year.

Source: S&P, eVestment, JP Morgan, Eckler calculations.

While Canadian investors benefited from a strong U.S. dollar in 2024, 2025 to-date has brought a reversal. As the Canadian dollar strengthens, the currency tailwind of unhedged USD exposure has turned into a headwind. While U.S. equities have risen 8.6% year-to-date through July 31 in local currency terms, Canadian investors with unhedged US dollar exposure have seen a gain of just 4.4%, as equity gains were partially offset by currency losses.

The importance of the U.S. dollar to Canadian investors

For most Canadian investors, the U.S. dollar represents their largest foreign currency exposure by a large margin. U.S. equities comprise two-thirds of global equity market capitalization, more than ten times the size of the next largest country, Japan. U.S. investments also account for a significant proportion of the investment universe in alternative asset classes, such as private equity, private debt and infrastructure.

Given the prevalence of U.S. assets in the investment landscape, the CAD/USD exchange rate is the most important foreign exchange rate pairing for nearly all Canadian investors. Canadian investors with unhedged exposure to USD-denominated investments experience gains or losses due to exchange rate fluctuations, independently of returns arising from changes in the asset’s local currency value. In 2024, a balanced portfolio consisting of 40% Canadian universe bonds and 60% global equities could attribute roughly one-third of its total annual return to USD appreciation.

The significant contribution of exchange rates to total returns in 2024 was by no means an aberration. Foreign exchange consistently plays a meaningful role in global equity returns. The table below illustrates the impact of CAD/USD exchange rate fluctuations on global equity returns for Canadian investors over the past 10 years.

Source: eVestment, MSCI, Eckler calculations.

In certain years – such as 2015 and 2018 – whether global equity returns were positive or negative depended on whether returns were measured from a Canadian dollar or U.S. dollar perspective.

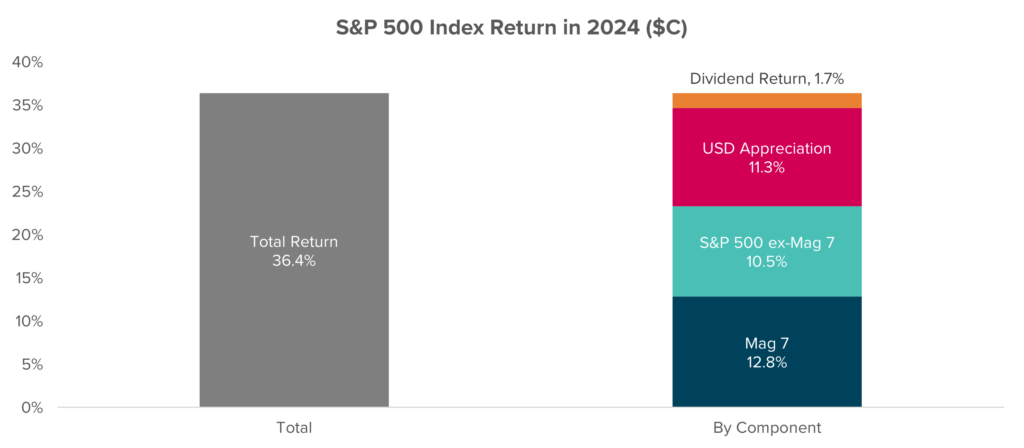

In 2025 to-date, the USD has depreciated relative to most currencies

As Canadian investors, we tend to view currency movements through the lens of whether the Canadian dollar has strengthened or weakened relative to foreign currencies. This framing makes sense, as exchange rate movements directly affect how much our dollar can buy when we travel or make a foreign purchase online. From this home currency perspective, the Canadian dollar has appreciated roughly 5.0% relative to the U.S. dollar since February 3rd. However, recent USD strength is more appropriately characterized as U.S. dollar depreciation rather than Canadian dollar appreciation.

Canada is not alone in experiencing USD depreciation relative to its home currency. Since the beginning of 2025, the U.S. dollar has weakened against many other major currencies, including the Euro, British pound sterling, Japanese yen and Australian dollar.

Source: LSEG Datastream. Data from January 1, 2024 through July 31, 2025.

Why the shift?

As a freely floating currency, the U.S. dollar’s exchange rate relative to other currencies is determined by supply and demand in the foreign exchange market. Recent U.S. dollar depreciation suggests that market participants have been selling U.S. dollars and buying foreign currencies.

Several factors have driven this USD outflow:

- Political and Geopolitical Uncertainty – Shifts in global alliances and trade relationships have led some countries to diversify away from U.S. trade and investment.

- Federal Reserve Policy Shift – The Fed began cutting interest rates in late 2024 in response to slowing economic growth and easing inflation. Lower interest rates reduce the yield on dollar-denominated assets, making them less attractive to foreign investors.

- US. Equity Outflows – Demand for U.S. dollars has been supported in recent years by capital inflows into the U.S. equity market, as many of the largest companies driving recent investment trends (e.g., Magnificent 7, Artificial Intelligence) are listed in the U.S. Periods of USD depreciation have often coincided with sharp sell-offs in these stocks.

Over the long-term currency effects are not material

As illustrated earlier, foreign exchange rate fluctuations can have a significant impact on returns over short periods, such as a calendar year. That impact, however, can be negative or positive. Over longer time horizons, year-to-year currency fluctuations tend to offset one another and total returns generally converge regardless of the investor’s home currency.

Source: eVestment, MSCI. Data to July 31, 2025.

Time horizon is therefore a key consideration for Canadian investors when evaluating currency exposure. Those with shorter time horizons may place greater emphasis on managing currency risk, while investors with multi-decade horizons can generally look through the short-term noise.

Key takeaways for Canadian investors

We’ve covered several foundational currency concepts in this article:

- The U.S. dollar is by far the most important foreign currency for most Canadian investors;

- Over the short-term, exchange rate fluctuations can have a material impact on foreign asset returns;

- Over the past 3 ½ years, U.S. dollar appreciation and subsequent depreciation have played a significant (and, we would argue, underappreciated) role in Canadian investor portfolio returns; however

- Over the longer term, foreign exchange gains and losses generally offset each other.

For investors concerned about short-term exchange rate volatility, establishing a currency hedging policy and implementing a currency hedging program can help reduce, or even eliminate, the currency-related component of investment returns. Hedging may be particularly attractive for investors with large short-term Canadian dollar-denominated liabilities or those subject to capital adequacy requirements that penalize unhedged foreign currency exposure, such as the insurance industry’s LICAT and MCT ratios.

For investors with longer time horizons, long-term annualized returns tend to be similar regardless of whether foreign currency exposure is hedged.

In both cases, however, understanding how short-term exchange fluctuations impact foreign asset returns remains valuable. Asset returns quoted in Canadian dollar terms conflate underlying asset returns with exchange rate volatility. Disentangling these two components can provide insight into how much of the return is driven by the appreciation of the underlying investments versus how much is attributable to the short-term (and generally mean-reverting) volatility of exchange rates.