Out with the old, in with the new… Canadian mortality tables

In brief:

- The Canadian Institute of Actuaries has released the CPM 2024 tables, expected to replace the CPM 2014 tables and reflecting more recent pensioner mortality experience in Canada.

- Key changes include new “Heavy” and “Light” tables based on occupation type instead of the previous public/private sector distinction, and the introduction of survivor tables for spouses.

- Analysis will likely be needed to adjust the mortality assumption for pension and benefits plans, and determine the associated impact, which will vary significantly depending on plans’ current mortality assumption and the demographic characteristics of the plan.

The Canadian Institute of Actuaries (“CIA”) recently released a report presenting the results of a multi‑year research project on mortality tables for Canadian pensioners (the “2026 Report”). The report introduces a new set of mortality tables – the CPM 2024 tables – which are intended to replace the CPM 2014 tables.

The CPM tables are widely used by pension and benefit plans in Canada, although alternative tables and modelling approaches are also applied in practice. The CPM 2024 tables provide updated, broad industry standards reflecting more recent experience and advances in mortality modelling.

The research underpinning the CPM 2024 tables was conducted by Ad Res Advanced Reinsurance Services GmbH, the same firm that developed the new Canadian mortality improvement scale released in 2024. We share Insights on the new improvement scale in our July 2024 and January 2025 articles.

This article summarizes the key characteristics of the CPM 2024 tables, highlights the main differences compared to the CPM 2014 tables, and illustrates the potential impact on life expectancy, annuity factors, and pension liabilities.

What’s new and what’s different in the CPM 2024 tables?

There are several important changes in the CPM 2024 tables compared to the CPM 2014 tables. Some of these changes are immediately apparent, while others reflect methodological enhancements that may not be obvious to users. The table below summarizes the key differences, with further discussion in the sections that follow.

| CPM 2014 tables | CPM 2024 tables | |

| Year of the tables | 2014 | 2024 |

| Experience period | 1999 – 2008 | 2011 – 2022 |

| Observed deaths during period | ~100,000 | ~300,000 |

| Tables published |

|

|

| Survivor tables | Not included | Included |

New methodology… .and a lot more data!

The methodology used to develop the CPM 2024 tables differs from that applied to the CPM 2014 tables. In addition, the CPM 2024 tables are based on a significantly broader cross‑section of Canadian pension plans, incorporating approximately three times the volume of experience data used in the development of CPM 2014. This richer dataset supports more robust results.

Goodbye Private and Public tables. Hello “Heavy” and Light” tables!

In addition to a combined table, the CPM 2014 tables included two sector‑based tables: one derived from private‑sector plans and another from public‑sector plans. This distinction reflected observed differences in mortality experience, with public‑sector members generally exhibiting longer life expectancies.

Since the release of CPM 2014, views on the appropriateness of a public‑versus‑private distinction have evolved. As discussed in an article published by Club Vita, differences attributed to sector can often be explained by other confounding variables. For example, some private‑sector plans are predominantly white‑collar and exhibit lighter mortality than many public‑sector plans, while certain public‑sector plans include groups with heavier mortality than those observed in parts of the private sector.

This observation is confirmed in the 2026 Report. As a result, the report does away with plan‑type distinctions and introduces two additional tables alongside the combined table:

- Heavy: based on data from plans with a high proportion of members engaged in heavy manual labour

- Light: based on data from plans predominantly comprising white‑collar occupations, particularly within the financial services and education sectors

No more pension adjustment factors

Mortality experience has long been observed to vary by socioeconomic status, with higher socioeconomic groups generally experiencing lower mortality rates. To approximate this effect, the CPM 2014 tables introduced pension size adjustment factors.

In practice, however, the use of these adjustment factors has been relatively limited. The 2026 Report notes that while pension size remains an important risk factor, it was not feasible to quantify mortality differences across contributing pension plans in a practical and consistent manner. Consequently, although the CPM 2024 tables are weighted by pension amount, separate tables by pension size have not been developed, and the use of pension size adjustment factors is no longer contemplated.

New survivor tables

One of the most notable innovations in the CPM 2024 tables is the introduction of separate mortality tables for surviving spouses. These tables reflect the higher mortality sometimes observed following the death of a retiree—a phenomenon referred to in the 2026 Report as the “grieving widow effect.”

The survivor tables are based on the observed mortality experience of surviving spouses of retired members. Separate survivor tables were not included in the CPM 2014 tables.

Lives-weighted tables

In addition to amount‑weighted tables, the CPM 2024 release includes lives‑weighted (unweighted) tables. These may be more appropriate for post‑employment benefit plans or pension arrangements where benefits are not directly linked to salary or pension amount.

Impact of the new tables

The impact of adopting one of the CPM 2024 tables depends on:

- Which CPM 2014 table is currently being used (Combined, Private, or Public), and

- Which CPM 2024 table is adopted (Combined, Heavy, or Light).

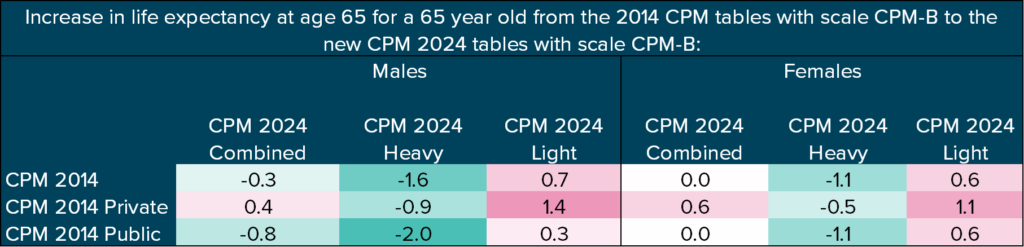

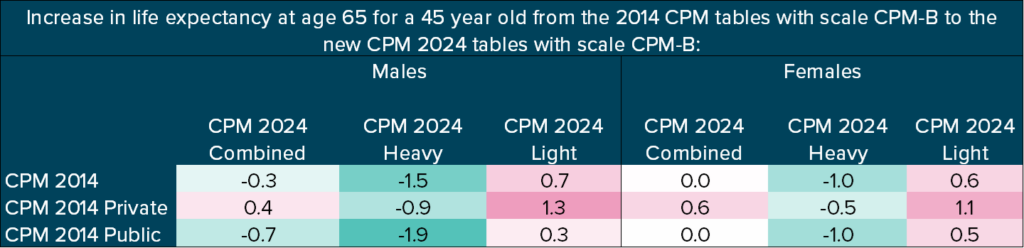

The tables below show changes in life expectancy at age 65, as at January 1, 2025, for individuals currently aged 45 and 65. Life expectancy is calculated using scale CPM‑B, which for now remains the most commonly used mortality improvement scale for Canadian pension plans. Decreases in life expectancy are shown in green, while increases are shown in pink.

Life expectancy results for individuals currently aged 45 are particularly relevant for funding and accounting valuations of active members.

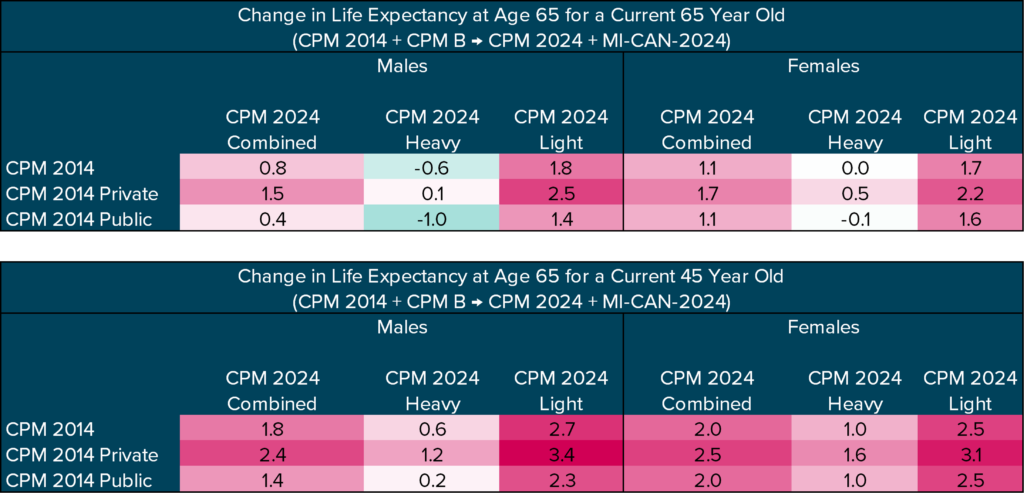

When the new MI‑CAN‑2024 mortality improvement scale is adopted in conjunction with the CPM 2024 tables, the combined impact on life expectancy becomes more pronounced. The tables below illustrate this combined effect.

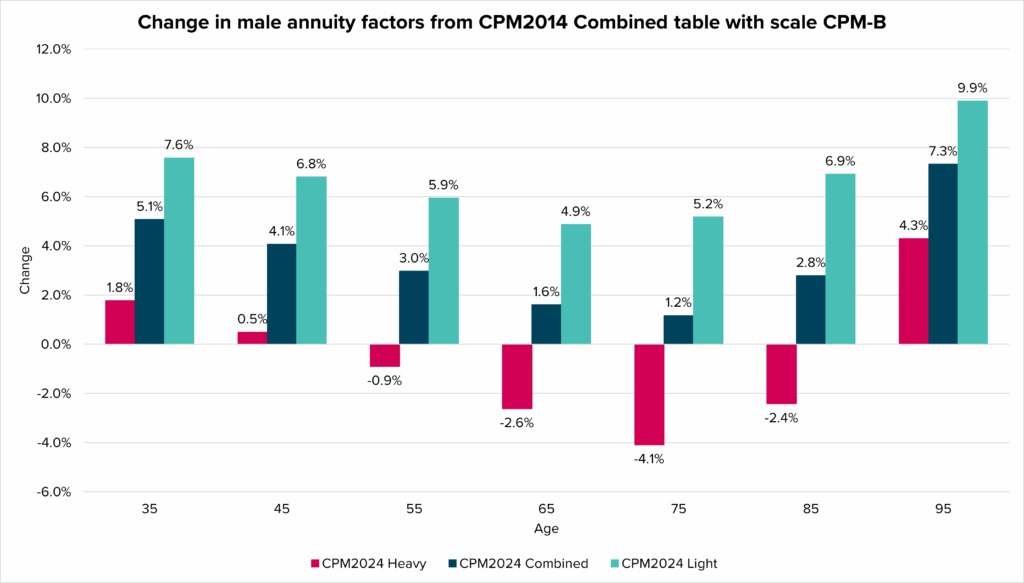

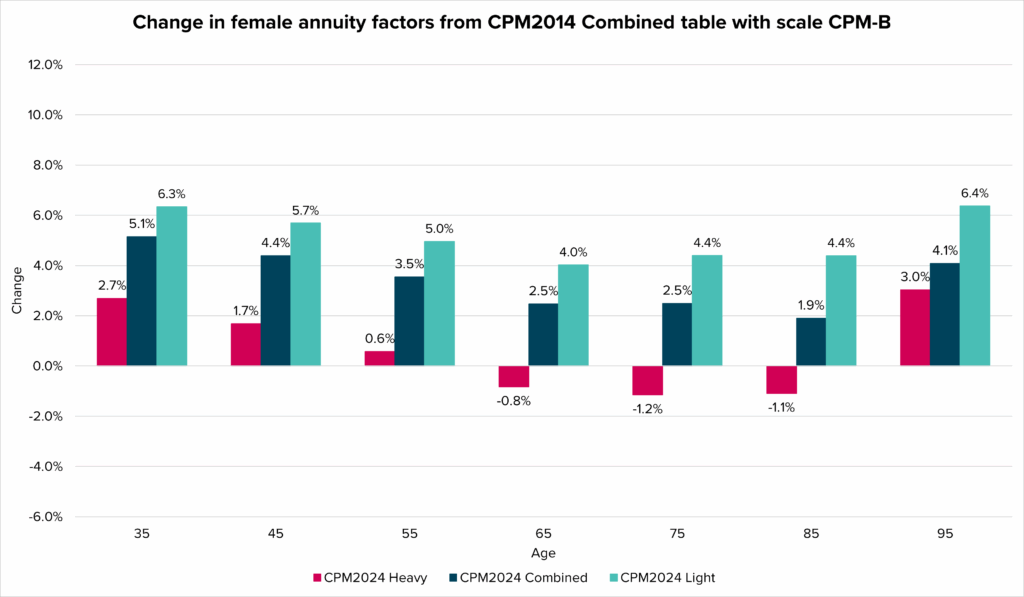

Impact on annuity factors

Consistent with the changes in life expectancy, the impact on annuity factors depends on both the table currently in use and the table being adopted. The charts below show the impact on annuity factors as at January 1, 2025 (deferred to age 65, or immediate if older), using a 4% discount rate, and MI-CAN-2024 improvement scale. Results are shown separately for males and females and incorporate adoption of the MI‑CAN‑2024 scale with the CPM 2024 tables.

The impact would generally be larger for plans currently using the CPM 2014 Private table and smaller for those using the CPM 2014 Public table.

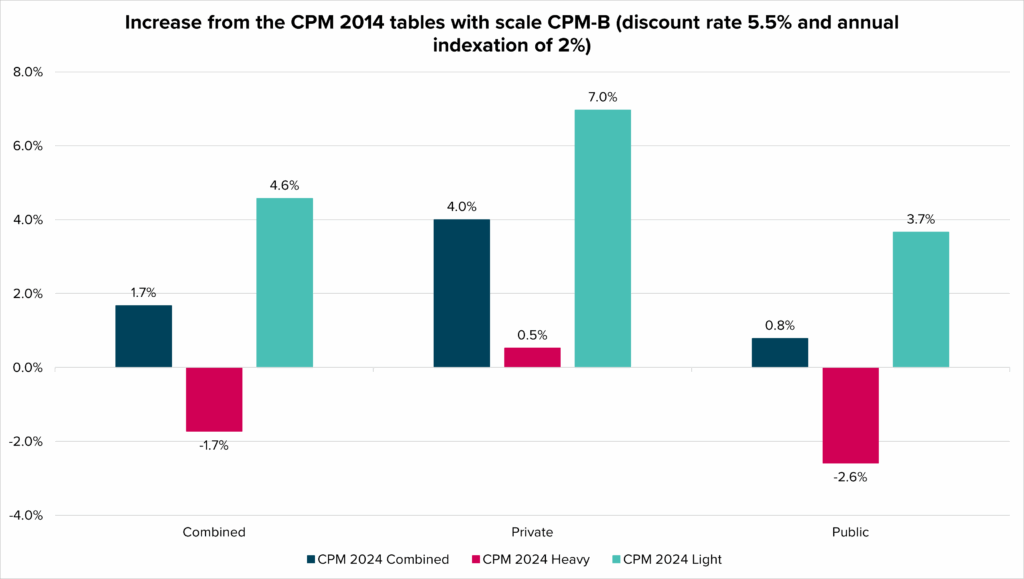

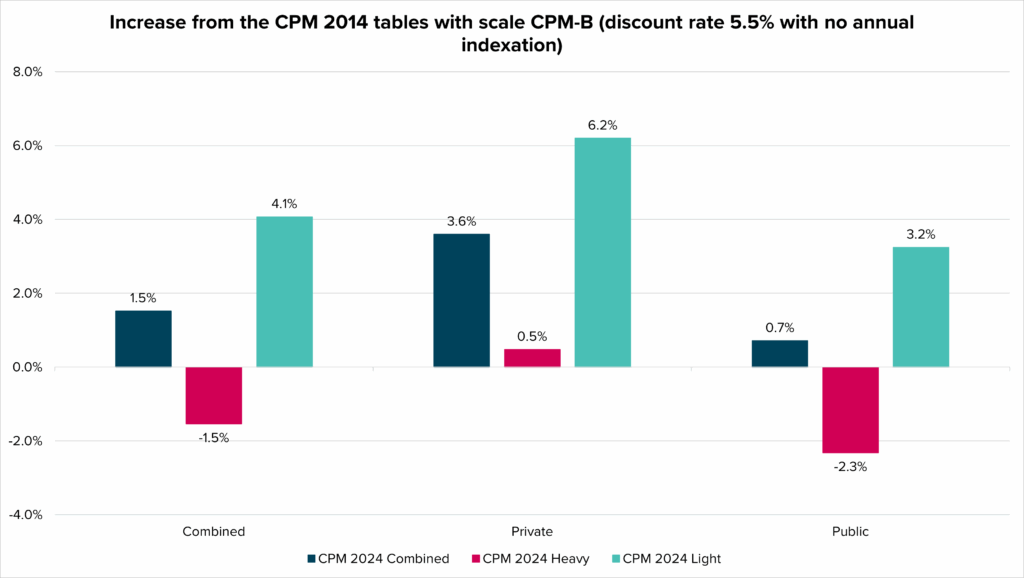

Liability impact

The chart below illustrates the impact of changing the mortality assumption from CPM 2014 with scale CPM‑B to CPM 2024 with the MI‑CAN‑2024 scale for a hypothetical pension plan. Results are shown with and without post‑retirement indexation, using a discount rate of 5.50%. Actual impacts will vary depending on plan demographics, benefit design, and economic assumptions.

Considerations for plan sponsors

As demonstrated above, the liability impact of changing mortality assumptions depends on both the current table and the table being adopted. When the new MI‑CAN‑2024 improvement scale is adopted alongside the CPM 2024 tables, it is more likely than not that liabilities will increase if either the Combined or Light table is selected.

What is the right table for a particular pension plan?

With the removal of the public‑versus‑private distinction, actuaries must now focus more directly on the nature of the work performed by plan members. Plans with a high proportion of heavy manual labour may be better suited to the Heavy table, while plans dominated by white‑collar employment in financial services or education may align more closely with the light table.

Challenges arise for plans that are not large enough to rely on their own experience or whose membership is not clearly heavy or light. For example, a financial services plan may include a wide range of socioeconomic groups, from highly compensated executives to lower‑paid support staff. In such cases, applying a single table to all members may require subjective judgment.

An alternative approach is to use a multi‑factor mortality model, such as Club Vita, which assigns members to different longevity profiles based on multiple characteristics. This can provide a more granular and potentially more accurate estimate of both individual life expectancy and total plan liabilities.

Considerations for survivor tables

Before adopting the new survivor tables, practitioners should carefully consider the following:

- The grieving widow effect may be temporary or permanent

- Survivor tables should only be applied after the death of the first spouse; using them earlier may understate liabilities

- Using non‑specific (“regular”) survivor tables remains acceptable, though liabilities may be modestly overstated

What’s next?

Following the release of the CPM 2024 tables, the CIA is expected to review the commuted value standards and consider whether to promulgate a new mortality assumption, potentially incorporating both the new tables and the MI‑CAN‑2024 improvement scale. The timing of any update remains to be determined.

We will continue to monitor developments closely and will provide further commentary, including any implications for commuted value standards, in a follow‑up article.

To learn more about this topic and the potential impact on your pension plan, please reach out to your Eckler consultant or contact us at: https://www.eckler.ca/lets-talk/